This analysis and discussion should be read in conjunction with the Financial Statements for the years ended December 31, 2018 and 2017 audited by Public Accounting Firm Purwantono, Sungkoro & Surja )a member firm of Ernst & Young Global Limited), which are also presented in this Annual Report.

According to Purwantono, Sungkoro & Surja )a member firm of Ernst & Young Global Limited), the consolidated financial statements of the Company received a fair opinion in all material respects, and were prepared in accordance with Financial Accounting Standard in Indonesia.

FINANCIAL POSITION REPORT

ASSETS

The Company’s assets consists of Current Assets and NonCurrent Assets, the composition of each asset as follows:

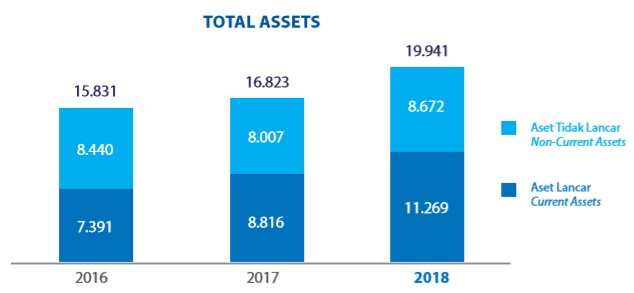

The Company’s total assets as of December 31, 2018 amounted to Rp19,940.9 billion, an increase of 18.5%, from Rp16,823.2 billion in 2017, due to higher cash balance from Rp1,771.2 billion in 2017 to Rp2,171.1 billion in 2018. Trade receivable also increased from Rp2,696.1 billion to Rp 4,404.6 billion, as average petroleum price increased during 2018. Total industrial estate land inventory also increased from Rp4,139.3 billion to Rp4,580.3 billion.

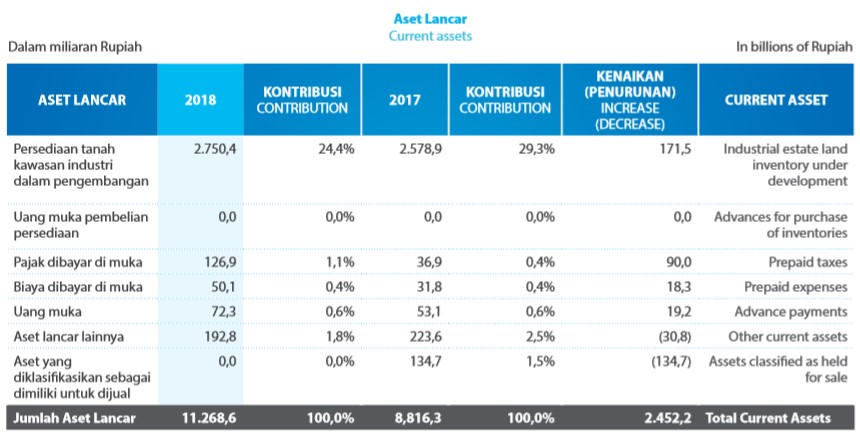

Current assets increased by 27.8% compared to the previous year to Rp11,268.6, due to a 22.6% increase in cash balance, inventory,additional industrial estate land inventory and trade receivable.

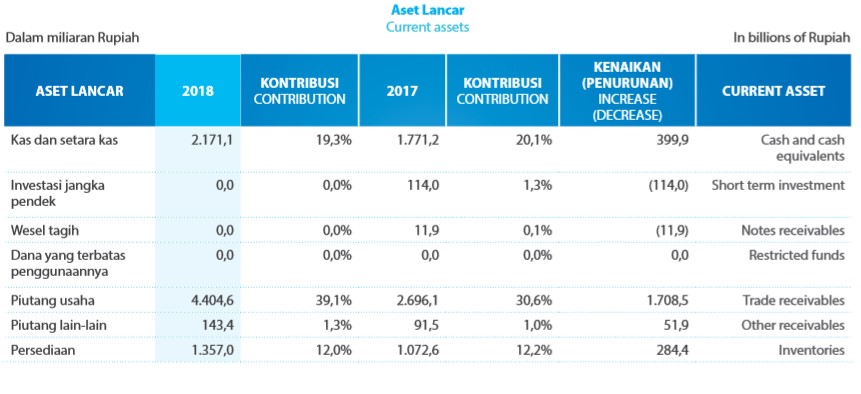

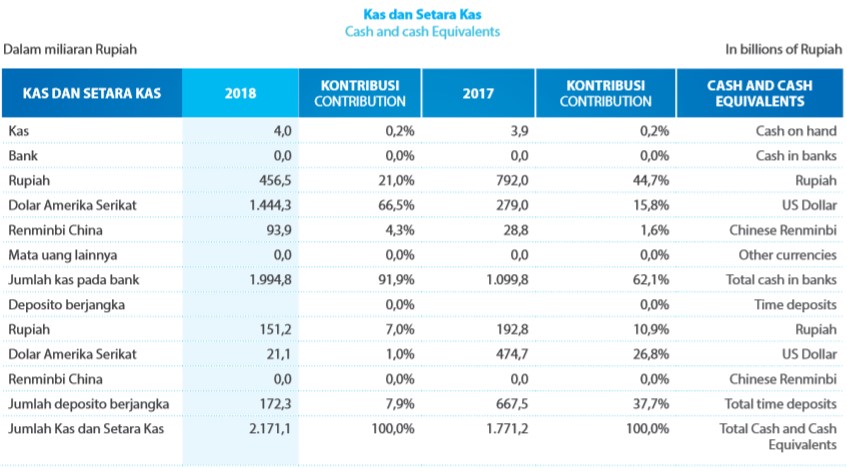

Total Cash and Cash Equivalents at end of 2018 amounted to Rp2,171.1 billion, an increase of Rp399.9 billion from last year. Of this amount, cash on hand amounted to Rp4.0 billion, cash in banks amounted to Rp1.994.8 billion, and time deposits amounted to Rp172.3 billion. The Rupiah time deposit rate was lower than 2017, ranging between 3.10% and 8.00% during 2018, while US Dollar deposit rates ranged between 0.60% and 2.00%, and Renminbi China deposit rates in 2.70% – 4.00%.

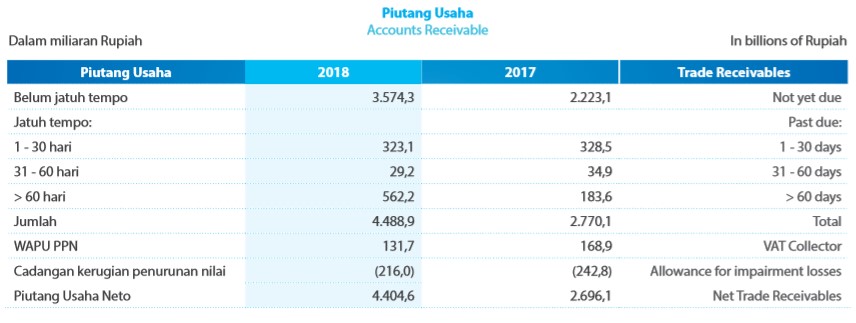

Accounts Receivable increased from Rp 2,696.1 bn in 2017 to Rp4,404.5 bn in 2018, as prices of petroleum and chemicals also rose during 2018. The Company continues to make effective efforts to reduce its receivables. These include tightening credit facilities to customers, cash before delivery, direct visits, and constantly monitoring and reviewing customers’ businesses.

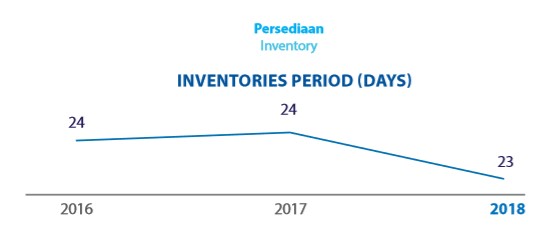

The inventory period decreased from 24 days in 2017 to 23 days in 2018. Inventories are covered by insurance against losses from fire, theft and other risks.

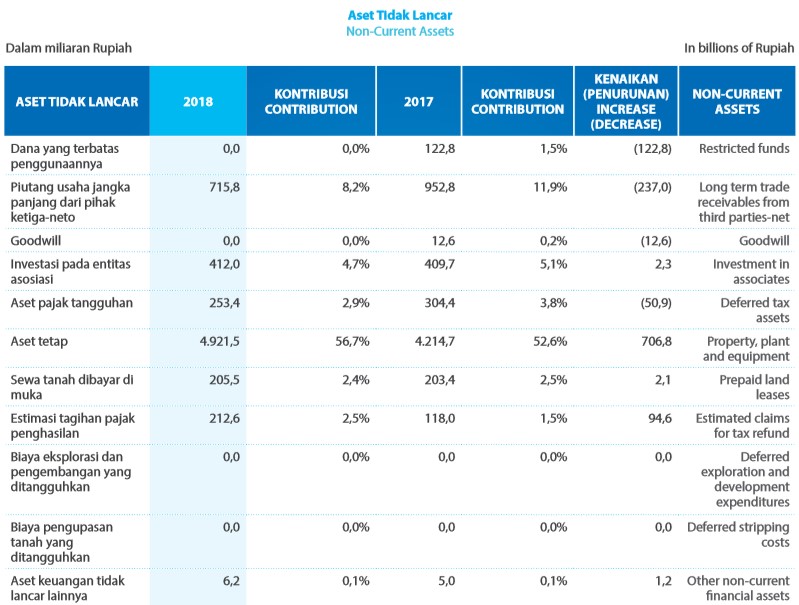

In 2018, Non-current Assets reached Rp8,672.2 billion, or a increase of Rp665.4 billion or 8.3% from 2017, mainly due to additional of Rp706.8 billion in fixed assets to Rp4,921.5 billion. Industrial estate land inventory under development also increased in amount Rp269.5 billion to Rp 1,829.9 billion.

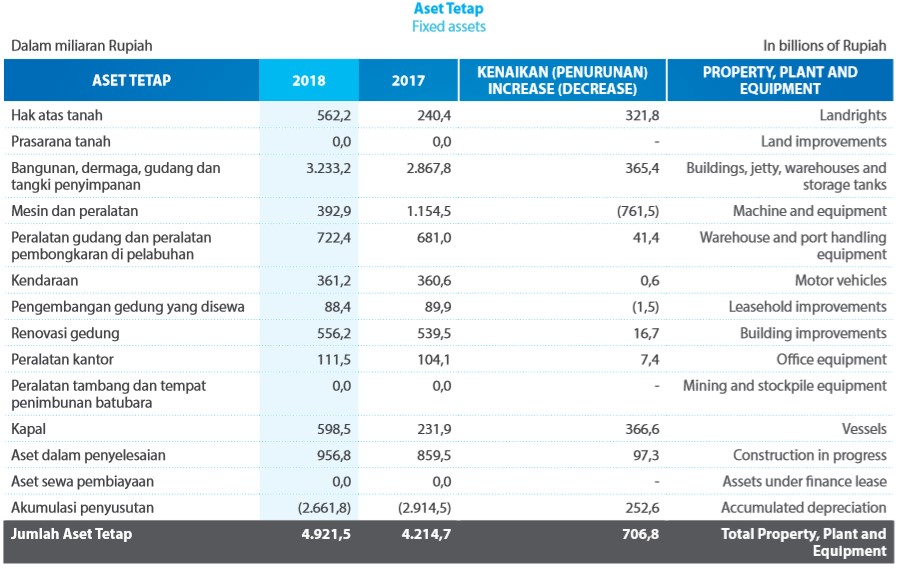

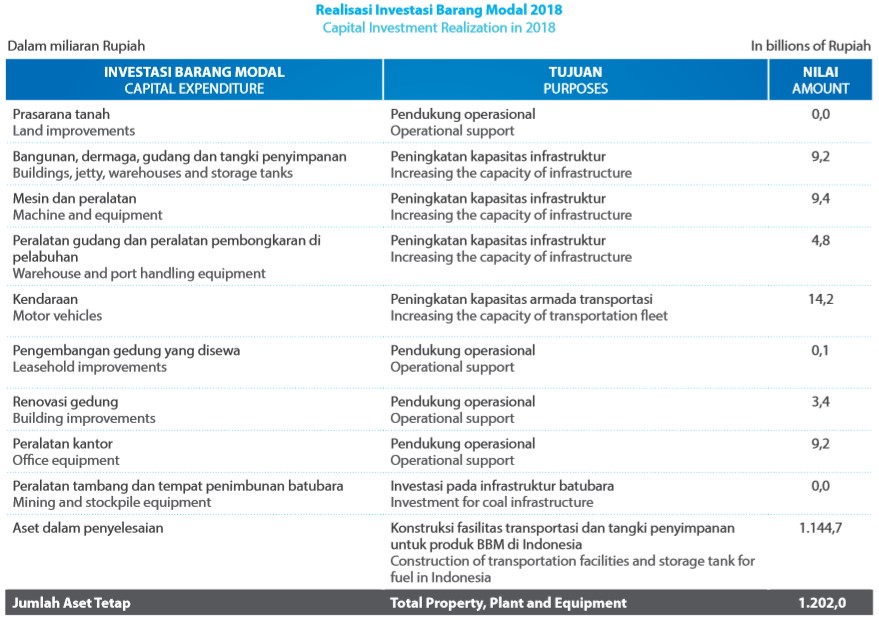

The Company’s fixed assets as of December 31, 2018 amounted to Rp4,921.5 billion, higher by 16.8% from Rp4,214.7 billion at the end of 2017. The increase in property and equipment was primarily due to the additional of construction in progress which represents construction of office building space, tank storage facilities, vessels, retail outlets for petroleum, with completion percentages ranging from 34% – 90% )December 31, 2017:24% – 95%). The construction of the above facilities is expected to be completed in approximately 1-2 years. The management does not expect any difficulties in meeting the targeted the completion dates.

Total borrowing costs capitalized by the Group in 2018 amounted to Rp56.9 billion )2017: Rp27.7 billion). The capitalized borrowing costs derived from general borrowings used to finance the construction of assets.

As of December 31, 2018, the acquisition costs of the assets which have been fully depreciated amounted to Rp928.6 billion )December 31, 2017: Rp783.2 billion). Those assets are still being used by the Group in operations.

As of December 31, 2018, the carrying amount of assets temporary not used in operations amounted to Rp93.7 billion )December 31, 2017: Rp106.8 billion).

As of the reporting date, the Management believes that the carrying amount for property, plant and equipment does not exceed its recoverable amount. Property, plant and equipment, except land rights, are covered by insurance against losses from fire, theft and other risks.

INDUSTRIAL ESTATE LAND INVENTRY UNDER DEVELOPMENT

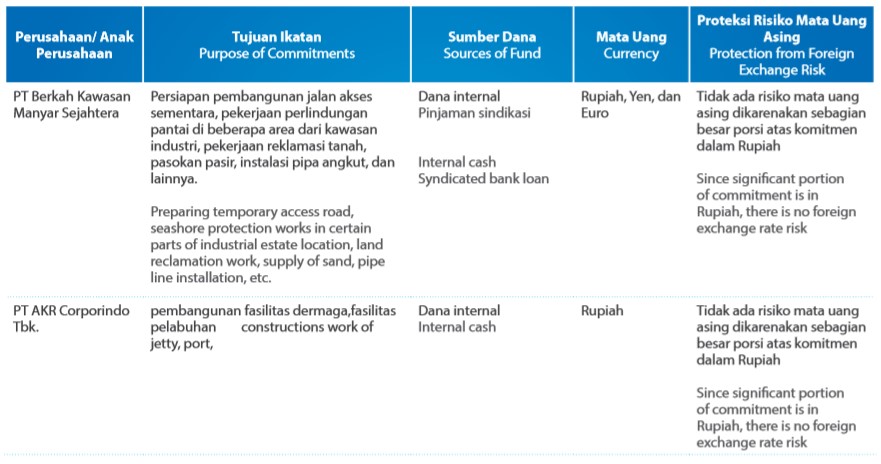

The industrial estate land inventory for development amounted to Rp1,829.9 billion, and were primarily land acquisition costs and related development costs, either directly or indirectly, including capitalization of loan of Rp152.0 billion with an interest rate of 8.65%. The capitalized land is located in Gresik and is being developed into an industrial estate for the JIIPE project.

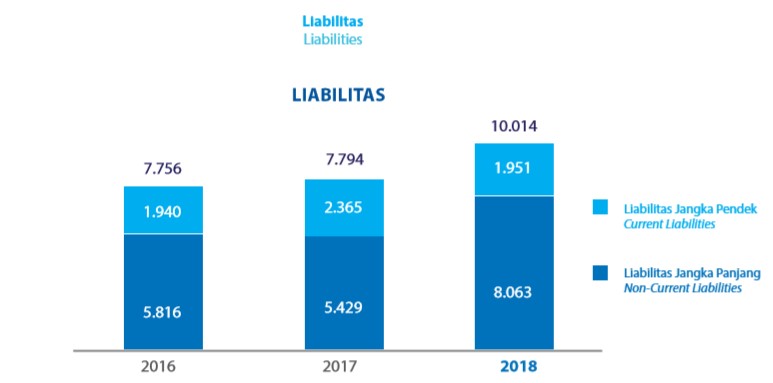

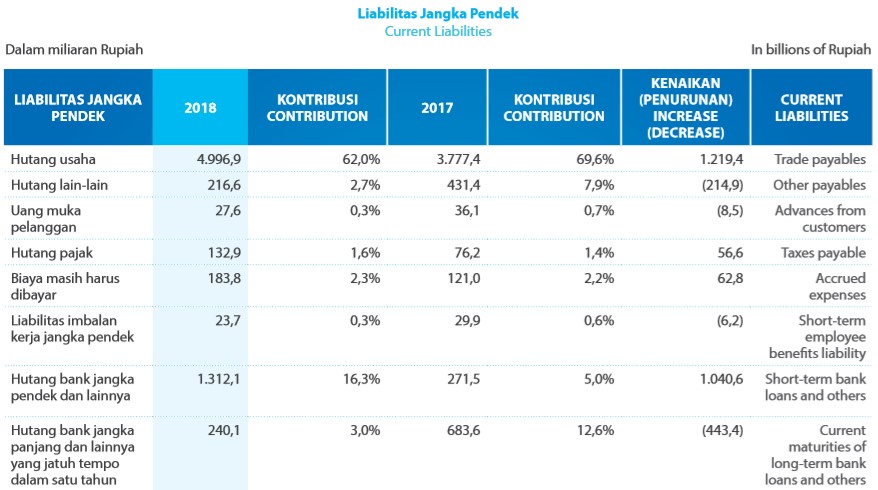

The Company’s liabilities at end of 2018 amounted to Rp10,014.0 billion, increased by Rp2.220.5 billion or 28.5% compared to 2017, due to the increase in trade payable and short-term loans. The short term loans are used for purchase of petroleum and chemical products )L/C facility), hedging, and tender projects.

Current liabilities at the end of 2018 amounted to Rp8,062.7 billion. This position was 48.5% higher than the Rp5,429.5 billion the previous year, mainly due to higher trade payable and short-term loans. It is in line with the growth in trading and distribution revenue

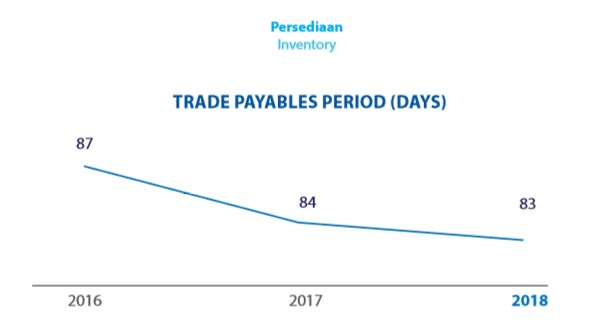

Trade payables by the end of 2018 increased by 32.3% when compared to the previous year, but the largest portion came from trade payable not yet due accounted Rp4,931.0 billion. Nevertheless, the current payables period has reduced to 83 days.

SHORT-TERM BANK LOANS AND OTHERS

Short-term bank loans and others increased from Rp271.5 billion in 2017 to Rp1,312.5 billion in 2018, mainly due to higher working capital loan of Rp1,041 billion. While short term loan related to JIIPE was recorded no change at; Rp120 billion.

CURRENT MATURITIES OF LONG-TERM BANK LOANS AND OTHERS

Long-term bank loans and others due within 1 year increased from Rp683.6 billion to Rp1,114,6 billion at the end of 2018, with the 2012 AKRA Bond of Rp874.5 billion is to mature in the following year.

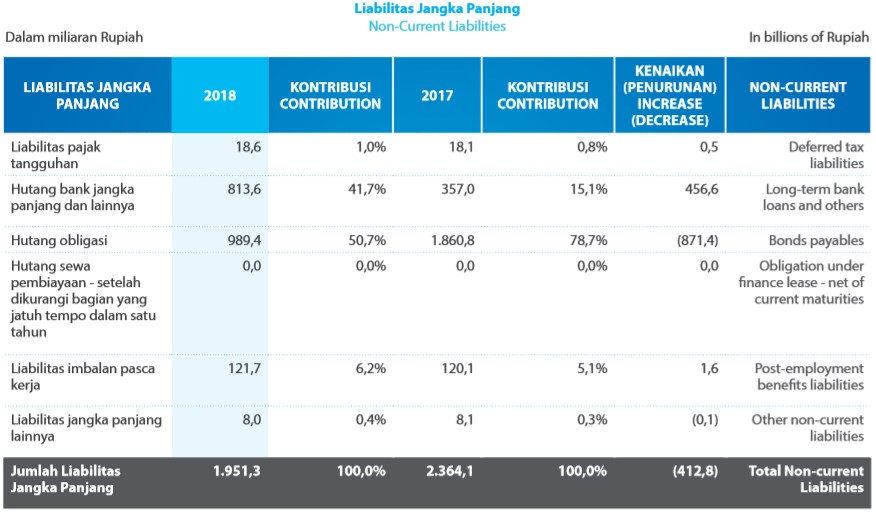

Non-current liabilities decreased by 17.5% compared to the previous year, as 2012 AKRA Bond is to mature the following year and now is recorded in current liabilities. The Company still has 3 types of bonds of 2017 with a total net value of Rp 989.4 bn

LONG-TERM BANK LOANS AND OTHERS

The Company recorded long-term bank loans and others amounting to Rp813.6 billion by the end of 2018, increased from Rp357.0 billion at the end of 2017. Higher long term bank loan mostly recorded in the subsidiaries level, including in,Andahanesa and AST.

BKMS Syndicated loan in amount Rp1,031 billion which was used to finance the infrastructure development of JIIPE projects in the industrial estate in Gresik, East Java, has been paid on 12 October 2018. The Syndicated loan of Rp211.6 billion, was planned to finance power generation projects of oil and gas )PLTMG). The Company also raised long term loan of Rp218 billion to finance the purchase of 2 units of vessel in 2018.

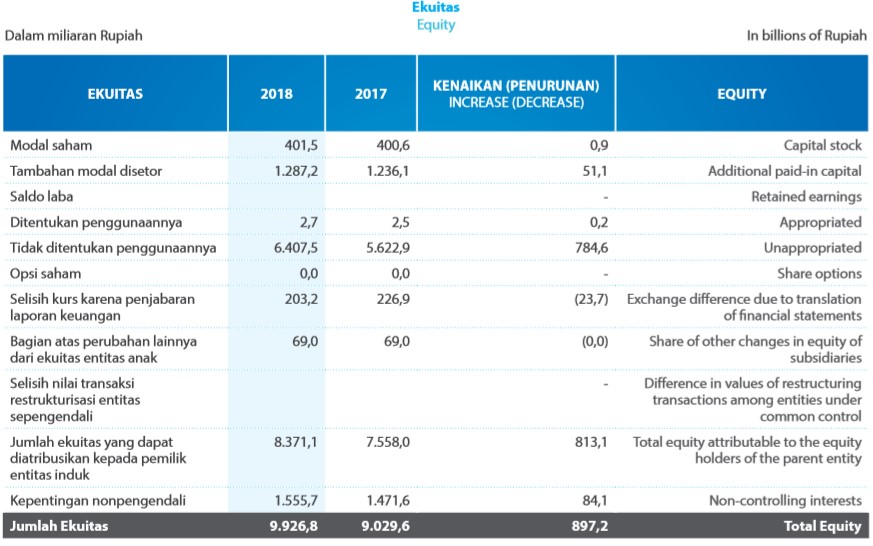

Total equity increased to Rp9,926.8 bn as of 31 December 2018 after retained earnings increase by 14 % to Rp 6407.5 bn compared to the previous year.

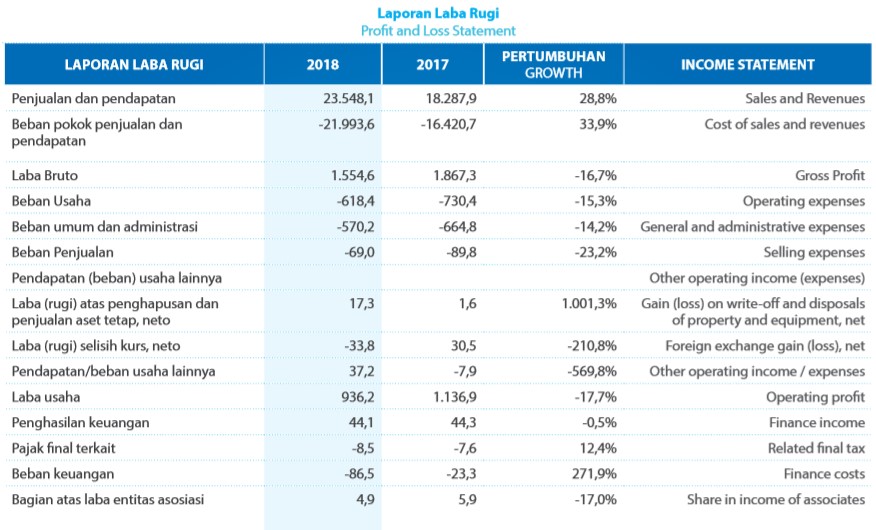

Net Profit of the current year attributable to the parent entity )the Company) in 2018 was Rp1,644.8 billion, an increase of 36.9% compared to 2017. The Company’s operating profit in 2018 decreased by 17.7% compared to the previous year, from Rp1,136.9 billion in 2017 to Rp936.2 billion in 2018.

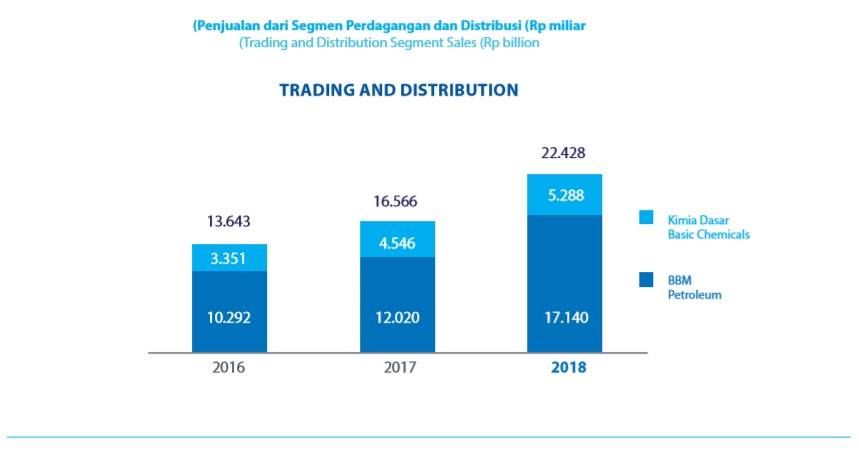

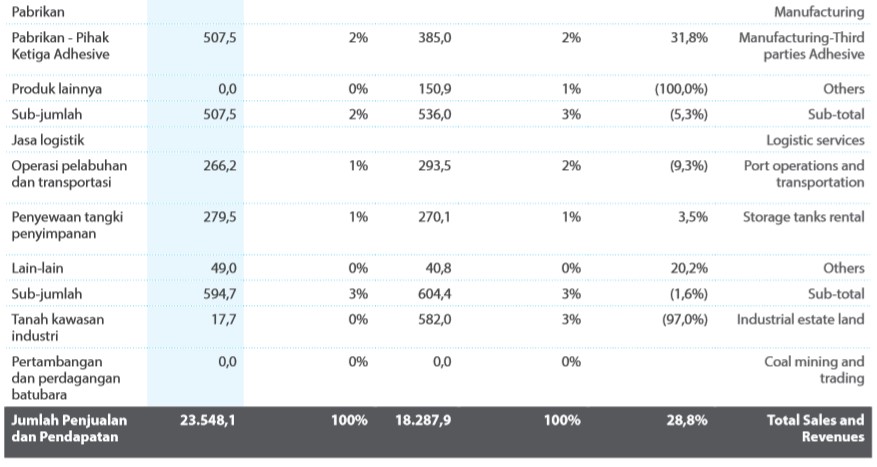

Consolidated sales and revenues increased by 28.8% to Rp23,548.1 billion in 2018. A sales and revenue analysis for each business segment is described in detail in the Operations Overview section of this Annual Report.

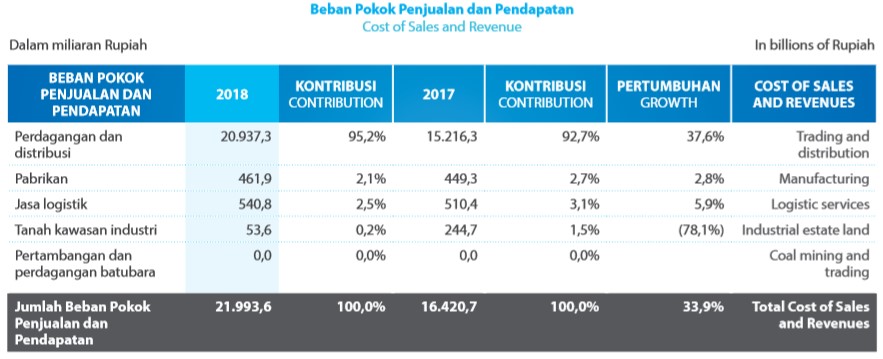

Cost of sales and revenues increased by 33.9% in 2018, from Rp16,420.7 billion in 2017 to Rp21,993.6 billion in 2018, primarily in the trading and distribution segment with Rp5,721.0 billion.

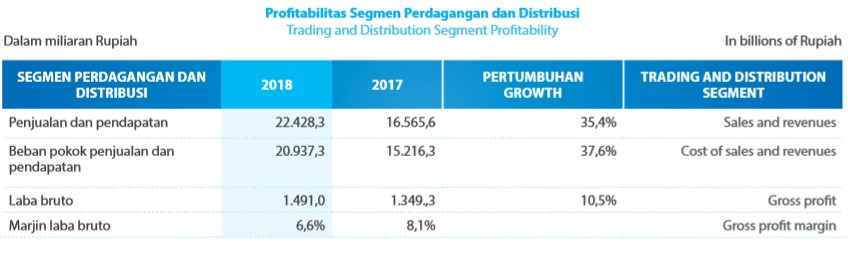

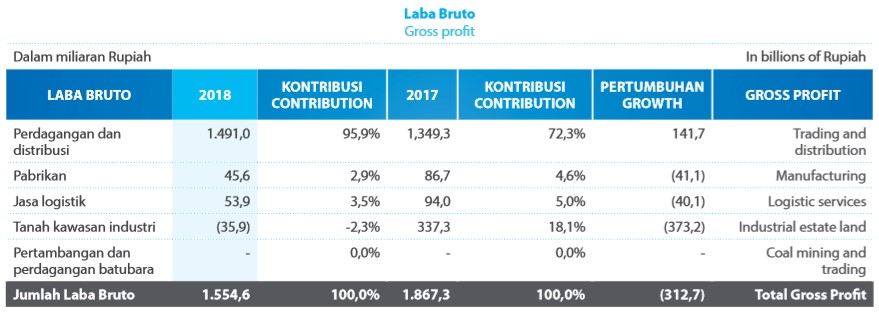

Gross profit in 2018 amounted to Rp1,554.6 billion, reduced by Rp312.7 billion compared to the previous year which recorded Rp1,867.3 billion. Trading and Distribution segment improved, but lower contribution from Industrial Estate reduced the overall gross profit.

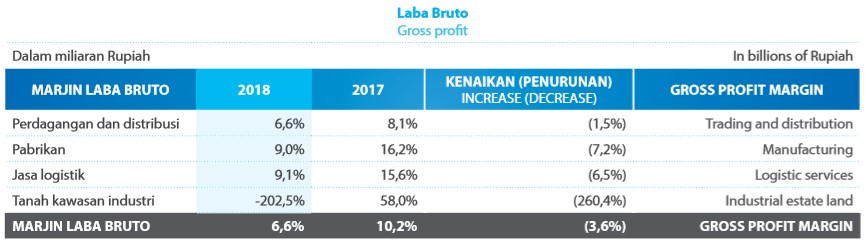

The trading and distribution margin decreased from 8.1% in 2017 to 6.6% in 2018 due to higher cost of sales and revenues, but total gross profit still increased. The consolidated gross profit margin also declined from 10.2% in 2017 to 6.6% in 2018.

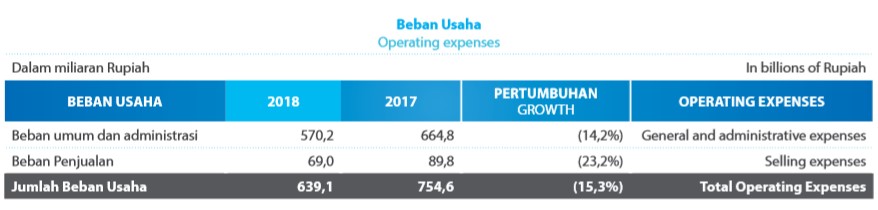

Operating expenses in 2018 decreased by 15.3% to Rp 618.4 billion compared to last year, due to lower GA expenses from Rp664.8 billion to Rp570.2billion. Based on ratio to sales, operating expenses percentage to sales declined from 4.3% in 2017 to 2.7% in 2018 .

FOREIGN EXCHANGE GAIN (IOSS)

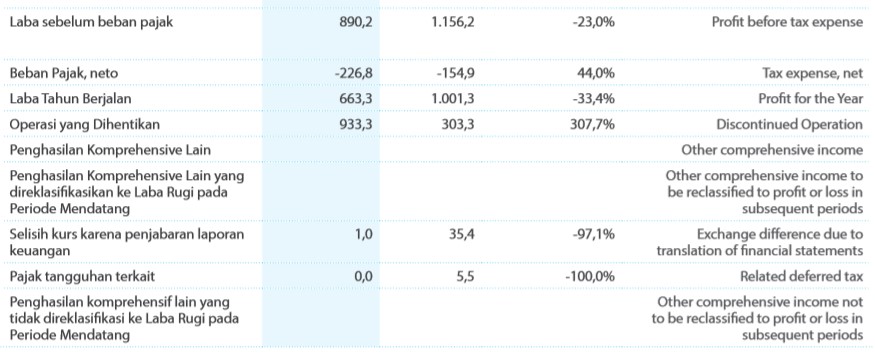

Foreign exchange losses in 2018 amounted to Rp33.8 billion, compared to gain of Rp30.5 billion in 2017. The USD exchange rate weakened by 6.9% from Rp13,548 in 2017 to Rp14,481 in 2018 and the RMB weakened by 1.8% from Rp2,073 to Rp2,110.

FINANCE INCOME (EXPENSE), NET

Net financing expenses amounted to Rp86.5 billion in 2018, increased significantly from Rp23.3 billion, due to increase in short term loans and long term loans as well as interest rates. The interest rate for short-term rupiah bank debt changed from 7.75% – 9.94% in 2017, to 5.95% – 9.94% in 2018, while for long-term rupiah bank debt it changed from 8.27% – 9.00% to 8.16% – 10.46%, respectively.

TAX BENEFIT (EXPENSE)

Net tax expense increased from Rp154.9 billion to Rp226.8 billion due to the increase in pre-tax profit.

DISCONTINUED OPERATION

Company recorded net profit for the year from discontinued operations of Rp933.3 billion from the gain of Khalista’s land sales and BKP divestment in 2018.

The Company recorded foreign exchange profit, due to the translation of the financial statements on the other comprehensive income reclassified in subsequent year, of Rp1.0 billion di 2018, compared to the previous year’s gain of Rp35.4 billion.

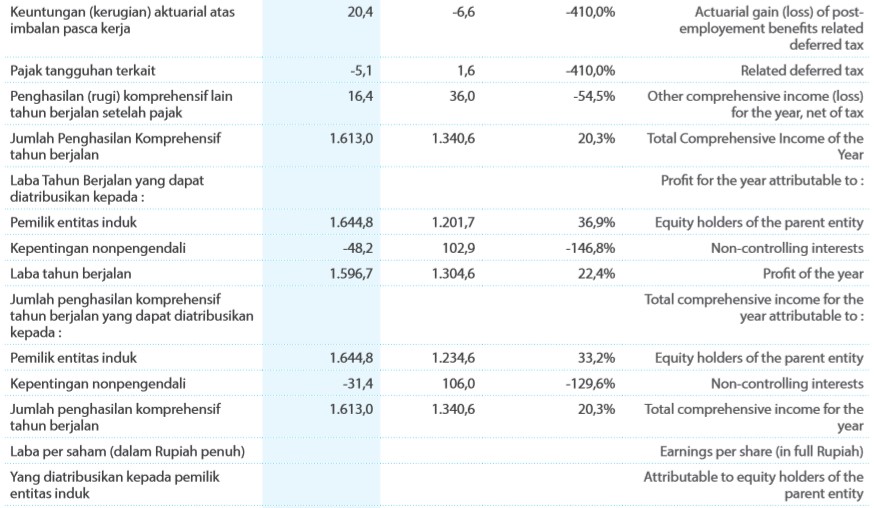

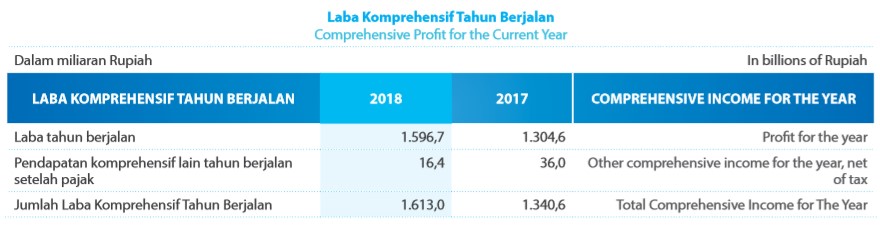

Other comprehensive income for the year came in at Rp 16.4 bn in 2018, helped by actuarial gain from post –employment benefit. Total comprehensive income for the year has increased from Rp1,340.6 billion in 2017 to Rp1,613.0 billion in 2018.

PROFIT OF THE CURRNET YEAR ATTRIBUTABLE TO THE EQUITY HOLDERS OF THE PARENTS COMPANY

The current year profit attributable to equity holders of the parent company increased from Rp 1,201.7 billion in 2017 to to Rp1,644.8 billion in 2018 with a net profit margin of 6.6%.

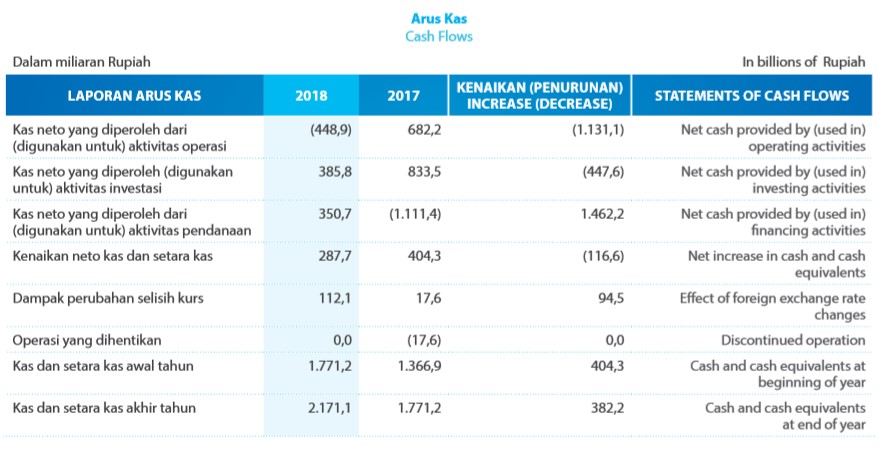

CASH FLOWS FROM OPERATING ACTIVITIES

Net Cash from operating activities decreased by Rp1,131.1 billion from Rp682.2 billion in 2017 to -Rp448.9 billon, due to higher working capital as on 31st December 2018.

CASH FLOWS FROM INVESTING ACTIVITIES

Most of the cash payments for investment activities were used for the acquisition of property and equipment amounting to Rp1,213.4 billion. Cash from investing activities was positive Rp385.8 billion following the Khalista land sales and BKP divestment worth Rp1,180.8 billion.

CASH FLOWS FROM FINANCING ACTIVITIES

Positive funding activities increased with the higher short-term loan for working capital in trading and distribution segment.

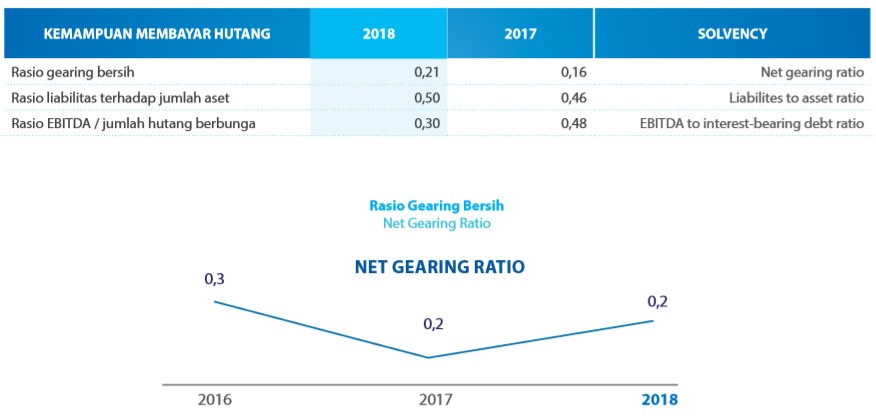

ABILITY TO PAY DEBT (SOLVENCY)

The Company’s ability to repay debt can be analyzed with three indicators, namely net gearing ratio, debt to total assets ratio, and EBITDA compared to interest-bearing debts.

With a cash balance of Rp2,171.1 billion, overall, the Company’s net gearing at the end of 2017 remained low at 0.21x in 2018, despite higher interest-bearing debts. The Company standsin a strong position to meet its debt obligation. Pefindo at the beginning of 2019 maintained its debt rating at “idAA-”.

LIABILITIES TO ASSETS RATION

At the end of 2018, only about 50% of the company’s assets were financed by liabilities, and this level has been relatively stable over the years. The Company’s assets are more than adequate to cover all debts.

EBITDA TO INTEREST-BEARING DEBT RATIO

The EBITDA to interest-bearing debt ratio was 0.30 times in 2018 compared to 0.48 times in 2017. This ratio indicates how high the EBITDA of the Company is when compared to interest-bearing debt. Interest-bearing debt, as presented earlier, increased at the end of 2018. With strong equity position, sound management, and increase in projected future earnings, Company’s default risk is expected to be lower.

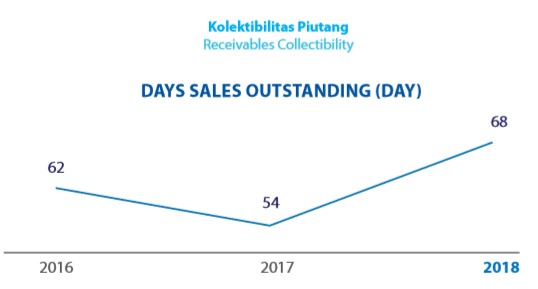

The average collection period for the Company’s trade receivables increased from 54 days in 2017 to 68 days in 2018. This occurred as a result of the increase in the Company’s revenue, and the increase in receivables past due >60 days. However, 81.1% of total net trade receivables, or Rp3,574.3 billion are still not yet due. Only about 12.8% or Rp562.2 billion are overdue for more than 60 days. Management took a prudent approach to receivables. Cumulatively, the Company has allocated Rp216.0 billion a reserve for impairment losses.

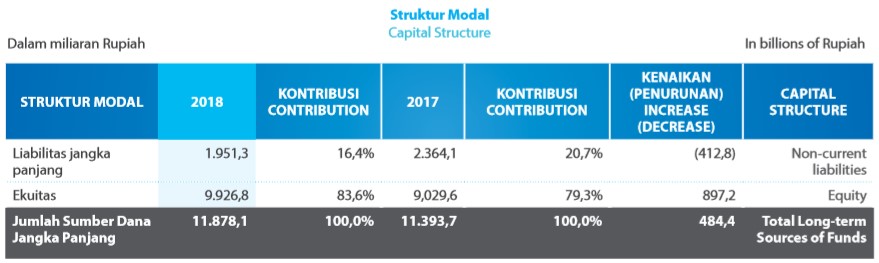

CAPITAL STRUCTURE AND CAPITAL STRUCTURE POLICY

The capital structure is a combination of long-term funding used by the Company. Long-term liabilities accounted for 16.4% of the Company’s long-term funding sources, while equity accounted for approximately 83.6%. The difference compared to last year was a decrease in the long-term liability percentage from 20.7% to 16.4% in 2018, and the increase in the percentage of capital from 79.3% to 83.6%, respectively.

CAPITAL STRUCTURE POLICY

The optimal capital structure to finance non-current assets minimizes the capital costs, maximizes shareholder value, and generates a good credit rating.

The Company is committed to creating shareholder value by maintaining a high return on equity ratio. Capital expenditure, and new projects, will be prioritized to be financed by internal cash, long-term debt, or bonds. The Company rarely conducts a rights issue as a source of financing. The Company also has certain ratio limits imposed by the Company’s creditors, such as the ratio of investments to equity.

MATERILA COMMITMENTS FOR CAPITAL INVESMENTS

COMPARASION OF TARGET AND REALIZATION 2018

SALES AND REVENUES

Sales and revenue increased by 28.8% from Rp18,287.9 billion to Rp23,548.1 billion, or 106% of revenue target. A sales and income analysis for each business segment is explained in detail in the Operations Overview section in this Annual Report.

PROFIT

The current year’s profit growth attributable to equity holders of the parent company increased by 35.9% compared to the previous year to Rp1,644.8 billion or 118% of profit target. The actual net profit margin of 6.6% was 0.4% above target. A detailed analysis of the profit increase has been explained earlier in the Financial Overview section of this Annual Report.

CAPITAL STRUCTURE

The Company’snet gearing ratio remained at low of 0.21X and provided a return on equity of 19.6% in 2018. In general, the Company did not experience any significant changes in capital structure during 2018, nor changed its policy on capital structure.

2019 PROJECTION

SALES AND REVENUES

The Company expects sales and revenue growth of 10%-15% in 2019 taking into account the growth in distribution and trade segment of fuel and basic chemicals, logistics, and the sales of industrial estate land in the future.

PROFIT

The Company expects to grow its operating profit in line with growth in revenue.

CAPITAL STRUCTURE

The Company does not plan to make significant changes to the capital structure during 2019, or change its capital structure policy. As of December 31, 2018, the Company recorded cash and cash equivalents amounting to Rp2,171.1 billion and a net gearing ratio of 0.21X.

DEVIDEND POLICY

The Company has no plan to make changes to its dividend policy. According to the Initial Public Offering prospectus in 1994, the Company will distribute a dividend of at least 30% of net profit from the previous year, if its profits exceed Rp50 billion.

MATERIAL INFORMATION AND FACTS SUBSEQUENT TO THE ACCOUNTANT’S REPORT DATE

The Company’s financial statements have been audited by Public Accounting Firm Purwantono, Sungkoro & Surja )Member of Ernst & Young). The audited report were signed and reported by Benyanto Suherman on March 14, 2019. No information or material facts occurred after the date of the accountant’s report.

BUSINESS PROSPECTS

OUTLOOK PETROLEUM DISTRIBUTION

As a distributor of fuel products in the Indonesian archipelago, AKR Corporindo has developed a robust business model with a strong and strategically located logistics infrastructure throughout Indonesia. The company has an efficient mechanism to overcome economic volatility, where changes in world oil prices and currency exchange rate fluctuations can be passed on to customers. The Company has an effective risk management system and manages its net open position effectively.

Company aims to manage its cost structures effectively, including improving its supply chain management, as well as manages the right procurement times to improve margins. Despite of tight competition and cost pressure in 2018, the Company still recorded healthy profit in the trading & distribution segment. Mining industry was improving during 2018. As of 1 September 2018, The government announced the mandatory use of B20 Biodiesel by all industrial and transportation end users with certain exceptions. AKR was allocated the highest quota of FAME amongst private companies.

AKR has built and strengthened its end-to-end supply chain and provides solutions to customers by delivering quality products and services from overseas fuel refineries directly into the customers’ hands.

The Company also see opportunities from B20 mandatory program. B20 usage is mandatory for all type of industrial users, with certain exceptions. Distributors to blend diesel with 20% Fatty Acid Methyl Ester )FAME) which has to be sourced locally in distributor’s own facility

We expect improving petroleum demand in 2019, supported by B20 regulation and higher demand from mining, power, and manufacturing sector.

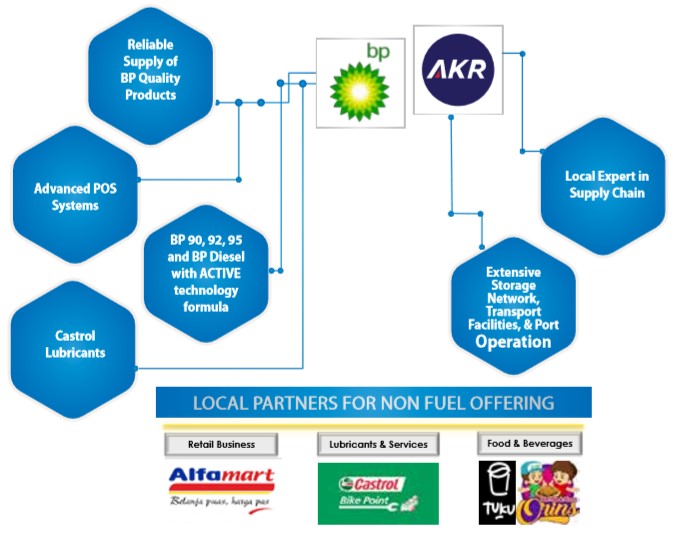

In retail segment, The Company is aggressively opening BPAKR petrol stations. First outlet has been launched in 2018, soon after JV agreement signed in 2017. Two Petrol stations of BP-AKR opened in 2018, and 4 more stations were opened in Q1 2019. It is strong and secure partnership that will deliver

differentiated offering to Indonesian consumers. We expect partnership with BP will give opportunities for retail fuel and non-fuel business.

With the strength of its logistics infrastructure, further strengthened by its partnership with BP for retail, the Company sees a positive outlook for a growth in fuel volume.

1. Mining

During 2018 the average of Newcastle coal price was around $92/MT increased by 3.8% from last year of $88/ MT. While the Indonesia Coal Reference Price reached $108.83/MT in August 2018. In February 2019, Newcastle coal price stood at $95/MT.

Despite of lower estimates for commodity prices due to continuation of trade war in 2019, IEA still forecasts that coal prices will remain stable over the next 5 years. The declining price in Europe and North America are offset by strong growth in India and Southeast Asia.

Indonesia’s coal production reached 548 million MT in 2018, representing an increase of 18.9% from previous year of 461 million MT, driven by expansion of coal production from several companies. It was higher than the government’s revised 2018 production target of 506.9 million MT. Of the 2018 production, 115 million MT was sold for the domestic market, up from 97 million MT in the previous year. Coal exports in the year reached 413 million MT, up 13.46% from 364 million MT in the previous year.

Despite of the export ban on mineral ores and commodity price fluctuation, the mining sector is still be the government’s mainstay until 5 years forward, mainly from coal, nickel, gold, copper, tin, iron ore, and bauxite. Also with a firm roadmap regarding the compliance of processing ore onshore the industry is much more stable now compared to a few years ago. Mining sector contributed 8% of GDP in 2018. Fuel demand from mining sector is still expected to grow in the future.

2. Power Plant

The company will also continue to supply fuel to the state-owned power plant. Although in the long-term power plants in Indonesia will be energyzed by steam, wind and water, but power plants that use diesel are still dominating. The Company is ready to support the diesel distribution that is needed for these power plants.

3. Plantation

The national palm oil industry performance was considered good in 2018. Total palm oil production in Indonesia increased 12% compared to the previous year and reached 47 million MT. Demand for palm oil is also supported by Biodiesel B20 mandatory program. In 2018, The Indonesian Palm Oil Entrepreneurs Association )GAPKI) recorded domestic absorbtion from biodiesel of 3.8 million MT, or increased by 72% from last year. GAPKI expected the palm oil production still growing in line with Indonesia economic growth. AKR customers from the plantation industry are mainly located in West Kalimantan, and in some areas of Sumatra.

4. Bunker Service

Mining bunkers and fishery bunkers use fuel from AKR. The prospect of fuel sales growth in the mining bunkers is certainly in line with the prospects for the mining industry. While the fishery bunker demand is determined by factors that influence the fishing activities such as weather, location, and policies related to marine and fishery management.

5. General Market

Indonesian economy in 2019 is forecasted to grow on the back of strengthening exports and investment. AKR hopes that the prospects for economic growth next year will also increase the raw material and energy needs for the manufacturing, trading, infrastructure and transportation sectors.

The infrastructure growth that being carried out by the government also presents a positive outlook for AKR petroleum revenue.

6. Ritel

The Company believes that the retail sector promises enormous potential. Currently, the ratio of petrol stations to the population of Indonesia is still very low. In addition, the increase in vehicle numbers each year is also quite high. The subsidies repeal for several fuel products, one being petrol, presented an opportunity for private players to participate in the petrol market in Indonesia. Since 2016, the Company began introducing AKRA 92 fuel, which has an octane level of 92. AKRA 92 sales are promising. With the operation of BP-AKR stations starting in 2018, the Company expects sales of high-octane gasoline to grow further.

In April 2017, the Company announced the signing of a retail joint venture in Indonesia with BP. The Joint Venture formed a company called PT Aneka Petroindo Raya, which operates under the name “BP AKR Fuels Retail”. In an exclusive agreement, both parties intend to develop and offer different experiences to consumers by leveraging the capabilities and expertise of BP and AKR in the emerging retail market in Indonesia. Two Petrol stations of BP-AKR opened in 2018, and 4 more stations were opened in Q1 2019. The retail sector will be a future growth factor for the fuel segment.

7. Subsidy

In the subsidized fuel segment, the Company only sells diesel. In January 2018, the Company has been assigned by BPH Migas as the Business Entity Implementing Agency for the Supply and Distribution of Specific Fuel for the next 5 years from 2018 to 2022. For year of 2019, AKR subsidy quota is 250,000 KL of diesel. It will be distributed through SPBKB and SPBN owned by AKR. In 2017 the Company began to participate in the Petroleum One Price Policy program. Up to January 2019, the Company has built 9 petrol stations as the agency of one price policy which located in area of 3T )The most Underdeveloped, The Frontest, and The Outermost). In 2019, the total of petrol stations for this program that will be developed by the company is 10 petrol stations.

8. Aviaton Fuel

In November 2016, the Company announced the signing of a joint venture agreement between AKR and Air BP. The joint venture, PT Dirgantara Petroindo Raya, operates under the name of Air BP-AKR Aviation, and was launched to develop the aviation fuel business in Indonesia. Indonesia is one of the fastest growing global aviation markets, where domestic travel is projected to grow ± 15% annually, reaching 180 million passengers by 2021. The Company expects government’s support for private sector participation in the aviation fuel.

OUTLOOK OF BASIC CHEMICALS TRADING & DISTRIBUTIN

The Government has set GDP growth target of 5.3% in its 2019 budget, a tad higher compared to growth of 5.17% in 2018. We expect the future GDP growth will also boost demand for consumer and industrial goods. The basic chemicals sales in 2019, as the basic raw materials for these goods, is expected to grow in line with the GDP growth.

The company expects the volume distribution of basic chemical products to increase in 2019 following higher number of chemical factories that need basic chemicals, and industrial customer expansion.Growth for chemical products is expected to come from rayon, alumina, soap, glass, tableware pipes, cables, and construction material from PVC, also chemicals factories that need basic chemicas.

OUTLOOK OF WOOD ADHESIVES MANUFACTURING

Property industry in Asia is forecasted in slow growth pace, especially if trade war between the US and China remains. China credit tightening policy will probably push more property holders to sell their assets to raise cash for business operations However, in 2019 there is a signal of the trade war ending. It is expected to be happened and impact to investment growth in Asian countries. The company expects growth in Asia property sector will also boost demand for wood adhesives. ARUKI is expecting market outside Indonesia such as Africa , Bangladesh , Vietnam , Malaysia , Myanmar , Sri Lanka

On the domestic market side, the wood adhesive market will be tighter in 2019. New customers will be followed by new players growth in the adhesive industry. In 2019, Aruki will continue its market expansion in composite panel boards in Java and Papua, where many new factories are emerging. The diversification of adhesive products in the form of powder )powder glue) also gives Aruki an opportunity to offer products outside Indonesia and outside Java and Papua. In 2019 Aruki will be more stringent in terms of raw material purchases, as oil prices is likely to increase again and hence drive up Methanol price. Prudent raw material purchasing is a key to gain future profit growth.

OUTLOOK OF LOGISTICS

The Indonesian government is focusing on accelerating performance and infrastructure development to build Indonesia’s competitive advantage in terms of logistics. Indonesia is an archipelago with high logistical needs, and the Company has logistics facilities throughout Indonesia. With a total of 10 ports, the Company is ready to support the trading and distribution business and service the logistical needs of third parties.

1. Fuel Logistic

In line with the positive expectations for fuel growth in 2019, both for industrial and retail customers, distribution and storage facilities for liquid bulk products will also increase. Through AKR Sea Transport )AST), the Company distributes cross-island fuel using Self Propelled Oil Barges )SPOB). During 2018, we have added 2 vessels, so the total of our vessels be 12 units. While land distribution is with trucks owned by AKR Transport Indonesia )ATI).

2. Jakarta Tank Terminal (JTT)

An expected increase in fuel imports will also increase demand for fuel storage tanks. Royal Vopak announced an expansion of 100,000 cbm for petrol and biofuel storage at PT Jakarta Tank Terminal )JTT), on February 16, 2018. This expansion will add 8 storage tanks with a total capacity of 100,000 cbm at the terminal, for gasoline, ethanol and biodiesel. The expansion will bring total JTT tank capacity to more than 350,000 cbm.

Strategically located in Tanjung Priok, the main port in Jakarta, JTT services the import and distribution market in the greater Jakarta area for fuel products. Imports of petroleum products, especially gasoline, have been increasing rapidly in Indonesia in recent years, and are expected to grow further driven by Indonesia’s economic growth and population growth. The demand for storage tank facilities is expected to increase both with the expansion of fuel distribution by existing players as well as with the entry of new players to the fuel market.

3. Bulk And Containers

The Company through Usaha Era Pratama Nusantara )UEPN) serves loading and unloading business in Surabaya.. As of December 2017, PT Berlian Manyar Sejahtera )BMS) has obtained a concession to carry out the operation of Terminal Manyar port services in Gresik Port, East Java for 76 years from the Ministry of Transportation

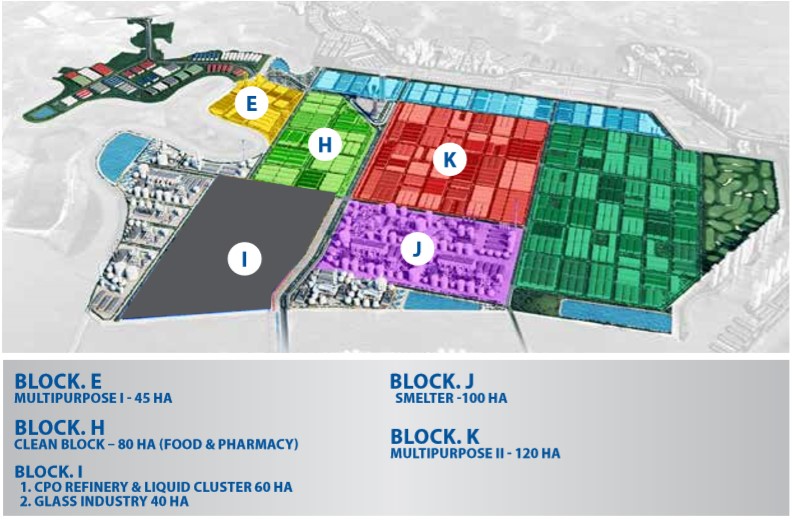

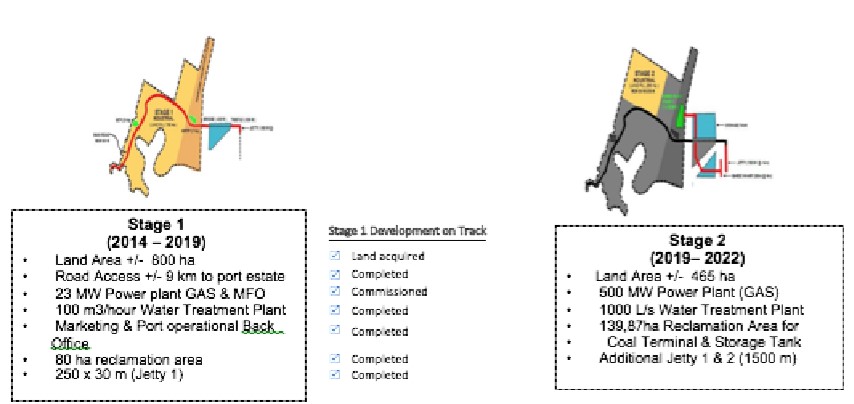

JAVA INTEGRATED INDUSTRIAL AND PORT ESTATE (JIIPE)

The Company believes that the industrial estate business will show a positive growth trend in the future, especially with the government’s support for economic development with significant infrastructure projects and development of Special Economic Zone )KEK). The Company and Pelindo III continue to develop the Java Integrated Industrial and Port Estate )JIIPE), and the industrial zone )BKMS) integrated with a deep sea port )BMS). In 2018, JIIPE was inaugurated as a National Strategic Project.

In 2019, JIIPE’s revenue is expected to increase with the land purchases by new tenants who will also use the supporting services prepared by the Estate management. By 2019, JIIPE’s targets include the following;

- Increasing the number of tenants

- Operational of Water Treatment and Waste Water Treatment Plant Gas Supply, and Internet Broadband Service

JIIPE has become a prospective source for future Company earnings. In addition to selling land, Company also provides electricity, water and logistics as recurring income. JIIPE is expected to support Indonesian companies to become global suppliers, while also supporting Indonesia in its contribution to the Economic Asean Community )MEA).

MARKETING ASPECTS

Petroleum

The marketing strategy for petroleum distribution business is as follows:

- Growing market share in the industrial sector by conducting intensive marketing and optimizing the network infrastructure more efficiently to the nearest customers’ locations, and improving service value to customers.

- Developing market in new areas, particularly in eastern Indonesia, and expanding storage capacity to be ready in handling in petroleum demand growth.

- Offering Vendor Managed Inventory )VMI) to create added value to key customers.

- Introducing and developing market opportunities for AKR retail business with BP as well as for aviation fuel products

Basic Chemicals

The basic chemical business is expected to grow in line with GDP growth. The strategy for the basic chemical distribution business is as follow:

- Increasing sales volume by grabbing new customers beside retaining current customers.

- Offering products to new customers in remote areas which located close to AKR storage tank

- Setting competitive price to offset customer sensitivity of future prices.

- Increasing the storage tanks capacity to prepare the demand growth that will be in line with Indonesia’s economic growth.

Wood adhesives Manufacturing

- Implementing competitive pricing for large potential customers

- Conducting intensive marketing for prospective customers who will build new factories in Java and Papua

- Offering and investigating the product overseas market

Logistics

- Improving and maximizing the dry and liquid bulk storage capacity in Indonesia

- Offering a “one stop service” for fuel and basic chemical customers

- Expanding tank storage capacity by 100,000 bcm to 350,000 bcm, together with Royal Vopak Joint Venture Partner, Jakarta Tank Terminal

Industrial Estate

- Targeting land sales to industrial tenants that need port facilities and utility services.

- Developing integrated industrial estate with facilities, electricity, water, and gas

- Generating utilities recurring income from current tenants

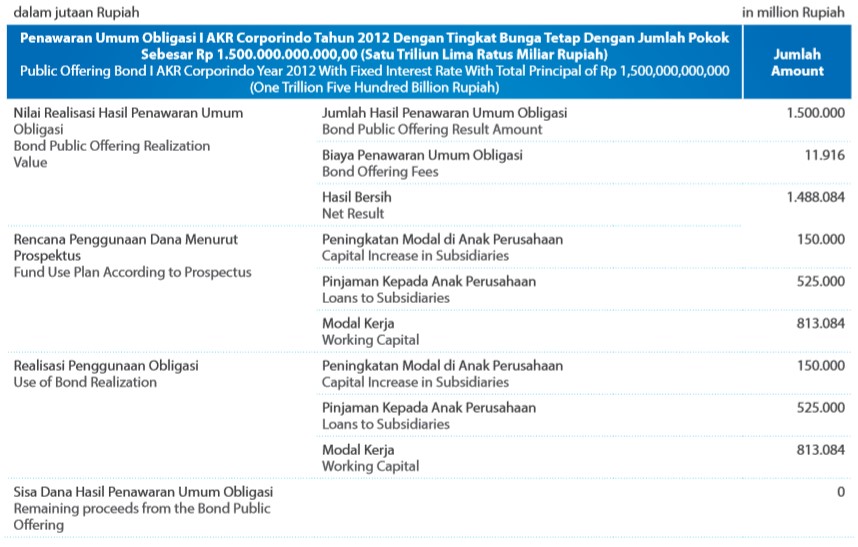

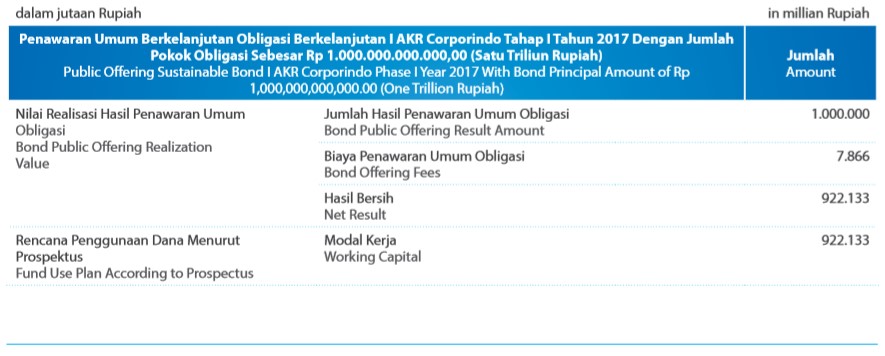

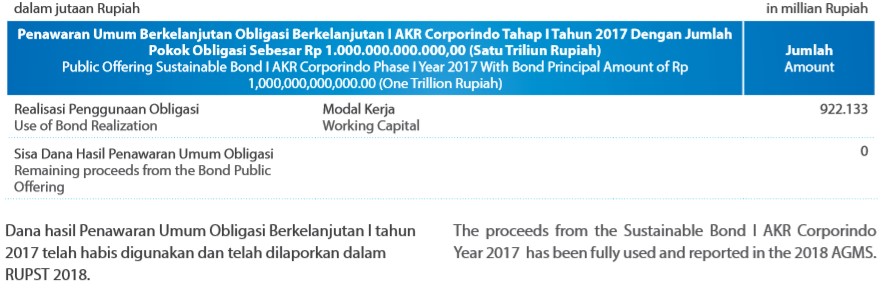

UTILIZATION OF PUBLIC OFFERING PROCEEDS

The proceeds of the bond issuance has been fully used and its use reported in the AGMS on May 5, 2015

The proceeds from the Sustainable Bond I AKR Corporindo Year 2017 has been fully used and reported in the 2018 AGMS.

MATERIAL INFORMATION

The Company did not conduct any material investments, expansions, divestments, mergers, acquisitions, or debt / capital restructuring during 2018.

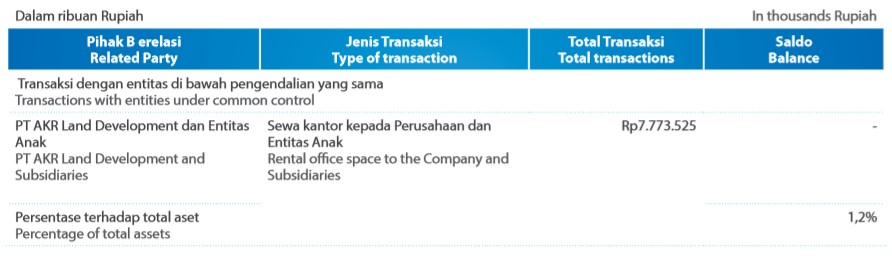

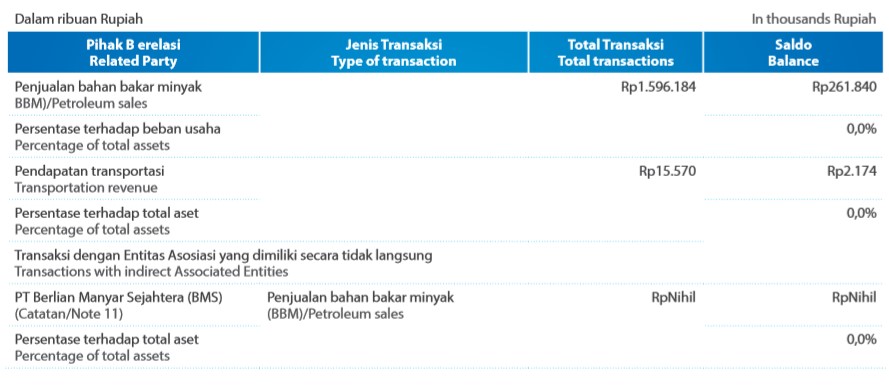

INFORMATION ON MATERIAL TRANSACTIOS CONFLICTS OF INTEREST AND/OR TRANSACTIOS WITH AFFILIATED PARTIE

In the normal course of business, the Company and Subsidiaries conduct transactions with related parties, which are carried out at the price level and terms agreed by the parties

CHANGES IN THE LAWAS AND REGULATIONS

As of 1 September 2018, all petroleum distributors in Indonesia required to distribute only B20 diesel to industrial user with limited exception.

CHANGES IN ACCOUNTING POLICIES

Effective on January 1, 2018, the following is issued accounting standard by the Indonesian Financial Accounting Standards Board )DSAK) that are considered relevant to the financial reporting of the Company and Group but has no significant impact on the consolidated financial statements:

- Amendment to PSAK No. 2: Statement of Cash Flows on the Disclosures Initiative. Earlier application is permitted. This amendment requires entities to provide disclosures that enable the financial statements users to evaluate the changes in liabilities arising from financing activities, including changes from cash flow and non-cash.

- Improvement to PSAK No. 15: Investment in Associate and Joint Venture. This improvement clarifies that at initial recognition, and entity may elect to measure its investment at fair value on and investment-per-investment basis.

- Amendment to PSAK No. 46: Income Taxes on the Recognition of Deferred Tax Assets for Unrealized Losses. Earlier application is permitted. This amendment clarifies that to determine whether the taxable income will be available so that the deductible temporary differences can be utilized; estimates of the most likely future taxable income can include recovery of certain assets of the entity exceeds its carrying amount.

- Amendments to PSAK No. 53 – Share-based Payment: Classification and Measurement of Share-based Payment Transaction These amendments aim to clarify the accounting treatment related to the classification and measurement of stock-based payment transactions.

- PSAK No. 67 )2018 Improvement): Disclosure of Interests in Other Entities This improvement clarifies the disclosure requirements in PSAK No. 67 also applied to any interest in the entity that is classified in accordance with PSAK No. 58.

The application of PSAK and other revised ISAK did not have a significant impact on the consolidated financial statements

In 2018, there were no issues that could potentially have a significant effect on the Company’s business continuity. The Company’s external and internal environmental conditions were still remained in a good position, even tend to be better than the previous year. Although in 2018 the exchange rate of Rupiah against US Dollar experienced fluctuations, the Company has a special strategy in dealing with these conditions.

In addition, the Company has a very good inventory and stock system, which was not affected by fluctuations in world oil prices.

The logistics infrastructure owned by the Company is also one of the Company’s strengths that are not owned by other players. With this strength, in 2018 the Company managed to realize an increase in net profit margin compared to the previous year.

ASSESSMENT CONDUCTED BY MANGEMENT

AKR Management periodically monitors the performance of the Company. Monitoring is carried out jointly with the Board of Commissioners and the Audit Committee. Based on the results of the monitoring, AKR Management concluded that the Company is still in a very good position and has great potential to continue to grow.

BUSINESS DEVELOPMENT POTENTIAL

The Company still has enormous potential for continuous growth. In the fuel segment, armed with the strength in logistics infrastructure that is further strengthened by a partnership with BP for retail and aviation fuel, the Company sees a positive outlook for the growth of fuel volume in the current segment and new segments.

In the retail sector, the Company will continue to encourage the development of its gas station network. The Company believes that the retail sector has a huge potential. Currently, the ratio of number of gas stations compared to Indonesian population is still very low. Besides that, the increase in number of vehicles every year is also quite high. To that end, the Company will continue to encourage the development of gas station network, both gas stations that use AKR brand )subsidized fuel and non-subsidized fuel) as well as BP-AKR brand )specifically non-subsidized fuel).

In addition, the Indonesian economy which is predicted to continue to improve in the coming years can increase people’s purchasing power and the economy will be moving forward again. This is an opportunity for the Company to spur the growth of basic chemicals and fuel volume.

AKR is keep developing Java Integrated Industrial and Port Estate )“JIIPE”) located in Gresik in East Java as one of Company’s expansion strategies. Through JIIPE, the Company providing logistics and energy solutions to industrial customers. The project will be one of the largest integrated industrial and port estates in Indonesia. JIIPE will make a better contribution to the Company in the future. Income from the sales of estate land and supporting infrastructure will be a new revenue source for the Company.